Reality bites: How managers perform under duress

There comes a time for every portfolio when conviction meets reality; when beliefs are tested by real-life stock market performance. So, how does a manager respond when a favoured stock falls 20% in value? Do they cut it immediately, wait for a turnaround, or double down and increase exposure Such conundrums aren’t rare, but the reaction to a share price decline says more about their skill level than any performance figures.

In this article, we analyse the response to valuation declines – and whether it’s possible to avoid holding losers too long or letting them go too soon.

Main takeaways

Declines are normal: One in three positions experiences a 20%

fall, but skilled managers can interpret that feedback.

Losses slow decisions: Once investors are in the red, reaction time slows. Positions kept after losses take longer to close out.

Patience can be a virtue: Stocks have a better chance of recovering if

they’re given time.

Conviction is crucial: High-conviction decisions will outperform. Managers who size and hold deliberately will demonstrate skill.

What happens when conviction is tested?

What happens if a fund manager’s conviction is properly tested? How will they react to a sudden stock price decline – and what can this mean for the portfolio?

Do they cut the position, keep everything crossed for an expected turnaround, or dig their heels in and buy more shares in an act of confident defiance? And what does their choice reveal about them as investors? That’s what we sought to find out by examining real-life decisions.

Our investigation

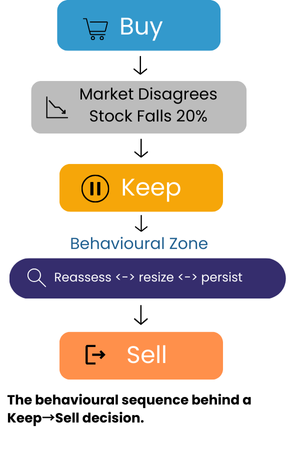

We analysed over 10,000 actual ‘Keep→Sell’ decisions. These occur when managers initially opt to maintain a declining position before cutting it from their portfolio. For this analysis, we focused specifically on cases where the position had already fallen 20% relative to the benchmark.

Our research, based on the SkillMetrics decision database, covered over 57,000 investment cycles across multiple equity portfolios. Each tracked the life of a position from its initial purchase to its eventual sale, including intermediate stages in which the manager decides to maintain or adjust exposure.

It allowed us to focus on the moments when the market disagrees, and the manager must decide whether to reassess, resize, or persist.

These are the seven insights gleaned from our research.

Insight One: Stress is common

About one in three decisions faces a 20% drawdown. Such drawdowns are a natural part of active fund management. They represent moments when the market challenges a manager’s thesis and forces a reassessment of conviction.

What separates the best managers from the rest isn’t the absence of pain, but how they interpret it. Some view it as information; others as a threat. If stress is common, the real question becomes how managers respond when the market pushes back.

Insight Two: Conviction under pressure

Conviction is revealed in the ‘Keep before Sell’ moment. Our research showed that thousands of decisions followed a behavioural sequence: the stock underperforms the market, the manager initially keeps the position, but eventually sells.

This illustrates real-world tests of conviction under stress. Each begins with the market disagreeing and ends with the manager resolving the situation. What happens in between is how conviction is managed.

Every Keep → Sell decision is a story of belief under pressure. In roughly two-thirds of cases, waiting led to deeper losses. In the remaining third, patience was rewarded. The manager's skill lies in recognising which story you are in before it ends. Conviction is valuable only when tethered to evidence.

After that initial decision to keep, another behavioural pattern emerges: delay.

Insight Three: Conviction under pressure

Losses make managers hold positions for longer. Once investors are in the red, every decision to act becomes harder. The result is a “delay premium” which sees conviction turning into persistence, and persistence into inertia.

Top-performing teams use structured review triggers. These are time-bound checkpoints following large drawdowns or resizing decisions, rather than binary keep/sell choices.

The longer the delay, the worse the outcome. Every day of hesitation compounds both the emotional and financial cost of being wrong. Yet delay isn’t always detrimental. Under certain conditions, time can work in a manager’s favour.

Insight Four: The time effect

Recovery odds rise steadily when patience is backed by fresh evidence. The probability of a recovery improves steadily over time. In fact, odds rise from 32% at the start to 36% within six months, 38% by one year, 44% over three years.

It shows that time can be an ally—when used deliberately. The odds improve the longer a position is held, provided the investment is updated as new information arrives. Therefore, investment managers who hold a stock for well‑founded reasons see their chances of a favourable resolution rise over time.

Their task is to ensure that this added time reflects fresh evidence, such as improving fundamentals, catalysts, or valuations, rather than mere hope. Even so, time alone isn’t a strategy. Both quick reactions and long waits carry risks.

Insight Five: No safe tempo

Acting fast can hurt, but so can waiting. While they benefited from the initial relief of exiting a poorly performing position, they also missed out on the rebound. Of the positions sold within a month of a 20% drawdown, 45% subsequently recovered, and those rebounds were, on average, 40% stronger than the continued declines of stocks that continued to fall.

However, those holding for longer also struggled. Only 35% of positions sold after three months and 36% after 12 months recovered before exit. Therefore, neither pure speed nor pure patience guarantees success. Skill in loss management is not about being right faster; it’s about learning faster and responding appropriately. And beyond a certain point, even the direction of the decision matters less than we might expect.

Insight Six: Stress flattens the outcome curve

When the market disagrees by 20%, patience and decisiveness are equally risky. Across thousands of analysed decisions, the outcomes converged.

About one-third of the kept positions recovered, while half of the quick sales missed out on rebounds. Neither side dominates consistently.

This challenges the idea that mechanical stop-loss rules eliminate behavioural biases. A blind 20% sell trigger would have forced exits on nearly half the positions that later recovered. Our research suggests that what managers need is structured re-evaluation: disciplined checkpoints informed by context, not by price alone.

When outcomes converge, the true differentiator must come from elsewhere, and that’s where conviction enters the picture.

Insight Seven: Conviction reveals skill

A manager’s belief is illustrated by the position they’re defending. As conviction (position size) rises, so does accuracy, asymmetry, and patience. Hit ratios climb from 29% to 53%, payoff quality improves and holding times lengthen. Larger positions are maintained for longer, reflecting informed patience.

Even among losing positions, managers who size up ideas recover more frequently, win larger amounts, and exhibit stronger asymmetry between success and failure. Low-weight looks like hesitation, whereas high-weight reflects conviction. Even in stressful conditions, managers allocate time and capital to where their informational edge is strongest.

Conclusion

Stock markets test conviction. When prices fall, every decision is made under pressure—and most investors shrink their edge when it matters most.

Our SkillMetrics data show that once a stock is down 20%, the likelihood of recovery decreases. Yet the odds improve steadily when conviction is backed by size and patience. The uncomfortable truth is that building conviction is the only real way out.

Managers who size decisively and think deliberately recover more often and win bigger. Conviction, when informed, is the last reliable signal of skill. In investing, the real differentiator isn’t who avoids stress, but who remains rational—turning conviction into clarity rather than comfort.

About:

SkillMetrics® revolutionises investment expertise by providing advanced behavioural insights tailored for portfolio managers. Our cloud platform identifies strengths, weaknesses, and behavioural biases, leading to improved performance. CIOs/CEOs can coach teams to enhance results by focusing on the investment process. Fund Selectors benefit from skill monitoring and behavioural diversification.

SkillMetrics® gives investment teams a clearer lens on the behavioural dynamics that shape outcomes — particularly how conviction is formed, tested, and expressed under duress. If you want to strengthen your team’s behavioural edge in moments of market stress, let’s discuss.