Forensic analysis: when performance can be linked to decisions

How do you know if the investment performances achieved are down to sound judgement or circumstance? Strong returns are traditionally seen as evidence of ability; disappointing results as proof of flawed reasoning.

But can performances be linked to the decisions that produced them – and what can these outcomes tell us about the approaches of institutional managers?

Main takeaways

Skill versus luck is the wrong question: ask instead whether performance can be meaningfully linked to the decisions that produced it

Decisions leave evidence behind: different types of decisions leave distinct fingerprints in outcomes and help explain how returns were generated

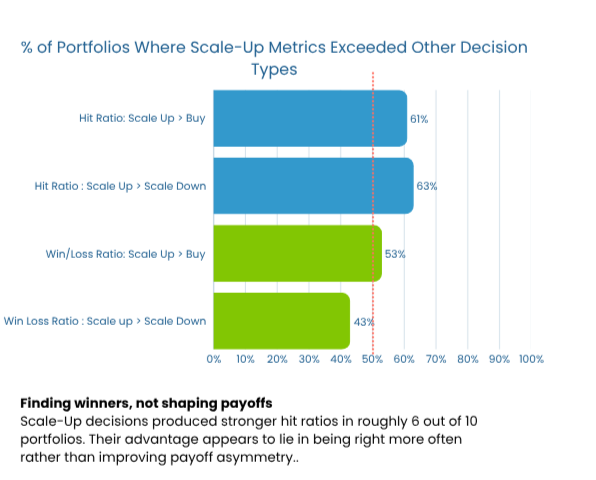

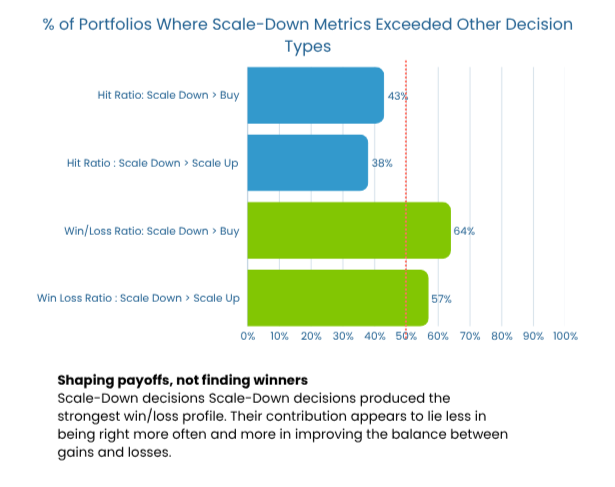

Different decisions achieve different objectives: scale-up decisions had the strongest hit-rate profile; scale-down the best win/loss profile

Combine with human experience: behavioural evidence is most powerful when combined with the manager’s explanation of their process and intent.

Why performance can be misleading

Most people jump to conclusions when evaluating results. If returns are strong, the manager is a genius; if they’re poor, then their process is weak. But the reality is more complicated. Managers can make smart calls and lose money, and generate returns from poor decisions.

Profitable investments can be down to well-timed increases in conviction, disciplined risk management, or simply a favourable backdrop. Stock markets are also influenced by countless factors beyond the investor’s control, such as geopolitical events, sector rotation and currency movements.

Looking beyond returns

This presents a challenge for allocators and investment committees. Performance is observed through outcomes, but understanding how those outcomes were reached requires examining the decisions that led to them. The reality is that similar outcomes can emerge from very different decisions.

To explore this relationship, we examined buy, scale-up, and scale-down decisions across 178 portfolios to compare how different decision types manifested themselves in outcomes.

Our research found:

Scale-up decisions exhibited the strongest hit-rate profile

Scale-down calls produced the strongest win/loss profile

Buy decisions showed neither pattern clearly

Taken together, these findings suggest that different decision types may reveal different dimensions of investment behaviour.

Let’s look at each in more detail.

Scale-up decisions

Scale-up decisions, where managers increased exposure, exhibited the strongest hit-rate profile. Our research showed that in about 60% of profiles, increasing exposure yielded a higher hit ratio than either initiating new positions or scaling down.

Interestingly, this advantage appeared primarily through hit ratio rather than win/loss ratio. In other words, scale-up decisions seem more closely associated with increasing the probability of success than with improving the balance between gains and losses. It could be that scale-ups represent engagement with an existing idea that has already been researched and monitored over time.

We also separated such decisions into momentum and contrarian contexts and found the former had stronger hit ratios in 53% of portfolios.

However, this is modest and can’t be explained solely by momentum. It may also reflect broader behavioural characteristics associated with increasing conviction.

Scale-down decisions

While they didn’t generate the strongest hit-rate ratios, scale-down decisions enjoyed higher win/loss ratios. This is consistent with the role they play in portfolio management.

Scaling-down decisions maximise upside while managing risk, recycling capital, and improving the balance between gains and losses.This means that their contribution appears less through forecasting accuracy and more via payoff efficiency.

Both scale-up and scale-down approaches can contribute positively to performance, even though they address different problems. While scaling up is more associated with increasing the probability of success, scaling down focuses more on shaping the balance between gains and losses.

Buy decisions

Buy decisions showed neither pattern clearly. They displayed a weaker hit-rate profile, alongside a positive, albeit less distinctive, win/loss profile.

Only 43% of portfolios achieved hit ratios above 50%, compared with 52% for scale-ups, according to our analysis.

One explanation is that buy decisions embrace various manager intentions, such as initiating conviction positions, building exposures, and implementing thematic views. Unlike scale-ups or scale-downs, they don’t appear to express a single dominant behavioural objective.

Why does this interpretation matter?

Choices made can reveal different types of investment behaviour and provide greater insight than purely focusing on returns.

Successful scale-ups and scale-downs can both contribute positively to performance, but they may reveal different qualities of the managers. For example, a scale-up approach could see them identify an emerging winner and increase exposure to the stock at the right time.

A successful scale-down, meanwhile, could have performed well even though the aim wasn’t to achieve additional upside but to reduce risk and protect capital.

That’s why performance can’t be interpreted accurately in isolation. The same outcome destination may have been reached via very different journeys.

The human factor

Understanding the intent behind the decision-making process requires discussions with the individual managers.

A scale-up may reflect growing conviction, but it could also be driven by a portfolio construction constraint or a response to changing information. Similarly, a scale-down could be due to deteriorating conviction levels as much as profit taking or prudent risk management.

The evidence generated by the data, therefore, becomes more meaningful once combined with the manager’s stated process.

Conclusion

Traditional performance analysis focuses on returns in isolation, but they’re only the visible outcome of a much larger decision-making process. The question isn’t whether performance was good or bad; it’s whether the outcome provides useful evidence about the behaviour and decisions behind it.

Scale-ups express themselves primarily through a higher probability of success, while scale-downs do so through payoff efficiency and risk management.

Understanding these can inspire investors to conduct more informed due diligence and gain a deeper understanding of how returns are produced.

About:

Investment performance is often evaluated through returns alone. SkillMetrics® helps managers and allocators go one step further by examining the decisions that produced those outcomes.

By analysing Buy, Scale-Up and Scale-Down decisions alongside behavioural patterns and portfolio context, SkillMetrics® helps identify the evidence that links performance to the underlying investment process.

If you would like to explore what your investment decisions reveal about the way performance is generated, we would be pleased to discuss.