Fixing the wrong problem: when the sell discipline isn’t at fault

Investors often blame bad sell decisions for bouts of poor performance – but what if they’re only the visible symptoms of deeper-rooted issues?

if the sell discipline isn’t actually flawed, then they could be wasting their time trying to solve the wrong problem and overlooking the real causes.

In this article, we examine whether the problems identified at the point of exit can actually be traced back to much earlier in the process.

Main takeaways

Don’t view sell decisions in isolation : poor performances may be due to upstream issues rather than a flawed exit process.

Poor starts leave a trace : positions in the weakest early-performance quartiles are more likely to exit at a loss.

Lifecycle struggles matter : repeated interventions suggest a position is

no longer behaving as initially expected.

Sell decisions provide evidence : they help reveal how the process is functioning across the investment cycle.

Misleading reactions

When exits are poorly timed, the natural instinct is to blame the sell discipline and look for ways that it can be improved.

It’s an understandable reaction. After all, the point of sale is visible and measurable. It’s where gains are made or losses realised. Treating it as a standalone factor persuades investors that results will improve if review points are tightened, price targets introduced or trimming policies formalised.

But these are purely downstream fixes that don’t guarantee success because similar exit frameworks produce different outcomes.

Limits to downstream fixes

The reality is that sell decisions don’t exist in isolation. They don’t begin and end at the time of the actual execution. They are the final step in a sequence. By the time a position reaches the point of exit, it carries the weight of all the micro decisions that have happened along the way.

That’s why you need to examine why it was originally selected, how the position evolved, and the number of times it was revisited along the way.

Revisiting sell discipline

We decided to examine whether extending the scope of an investor’s sell discipline can uncover patterns that influence the consistency of outcomes.

Around 27,000 sell decisions were analysed across 180 portfolios to see if the issues identified at the exit had appeared earlier in the lifecycle of the position.

Two key conclusions were drawn: bad endings often start with bad beginnings; and struggles during the lifecycle do matter. Let’s explore both in greater detail.

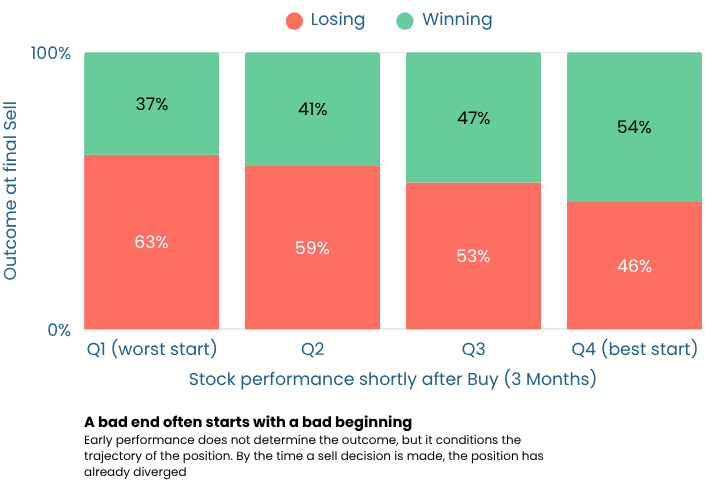

Bad endings start with bad beginnings

We grouped positions based on their performance in the three months after the initial buy and then looked at whether the eventual sell was at a gain or at a loss.

Positions in the weakest early-performance quartile were exited at a loss in 63.14% of cases, compared with 46.27% for positions in the strongest quartile.

This means positions in the weakest early-performance quartile were more likely to exit at a loss. Conversely, those in the strongest early-performance quartile had a greater chance of making a profit. While a strong start doesn’t guarantee success, it shows that early performance conditions can often affect the pathway it takes.

It affects the context in which future decisions are made and leaves a trace that resurfaces at exit.

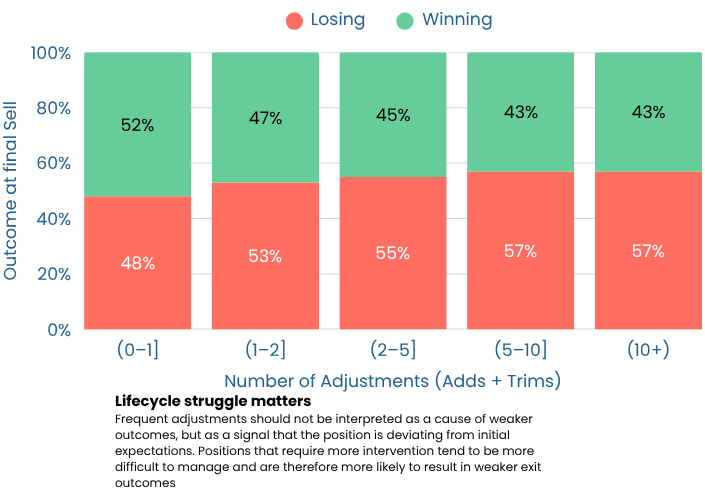

Lifecycle struggles matter

We looked at how often positions were adjusted before they were ultimately sold. This included additions and any trimming.

Positions with more frequent adjustments were more likely to be exited at a loss, whereas those with fewer appeared more balanced.

While adding to positions and trimming them is a normal and necessary part of portfolio management. It doesn’t mean intervention is inherently bad. The point is that repeated intervention is often a sign that a position is no longer behaving as initially expected.

Frequent adjustments leave a trace. They reveal that the position required more attention, more revision, or more active management during its lifecycle.

Is it time to look upstream?

Sell decisions remain important, of course, but our analysis shows they shouldn’t be viewed in isolation as other factors play a part. It’s not just the point of exit but how a position behaved shortly after it was bought and the amount of intervention it subsequently required.

As sell decisions contain traces of earlier decisions, trying to implement downstream fixes won’t be enough on their own.

What do sell decisions provide?

Investors must look at what sell decisions reveal about how positions are bought, their size, and the process of monitoring and adjusting positions?

This can:

Strengthen idea framing

Making conviction explicit through sizing

Defining payoff profiles more clearly

Monitoring how positions evolve

Conclusion

Sell discipline matters but it doesn’t begin at the moment of exit. The journey to this point will have started further upstream.

By the time a position is sold, it already carries the traces of its lifecycle: the way it started, the way it evolved, and the way it was managed over time.

The value of a sell decision lies in the path that led to that decision and exposes parts of the process that may need addressing.

About:

Sell discipline is often assessed at the point of exit, but many of the traces visible there are formed earlier in the investment lifecycle.

SkillMetrics® helps managers examine how positions are initiated, monitored, adjusted, and reassessed before the final sell decision. This makes it possible to diagnose upstream process patterns rather than focusing only on downstream outcomes.

If you would like to explore what your sell decisions reveal about the wider investment process, we would be pleased to discuss.