Idea generation: how the flow of ideas shapes portfolio behaviour

Portfolio analysis often focuses on structure and outcomes. This means examining how positions behave and how outcomes unfold. These are downstream expressions of the investment process - but less attention is paid to how those positions enter the portfolio in the first place.

In this article, we examine how idea generation influences portfolio construction, manager behaviour, and drawdowns.

Main takeaways

Idea volume carries limited signal: portfolios generating frequent new ideas don’t exhibit materially higher hit ratios.

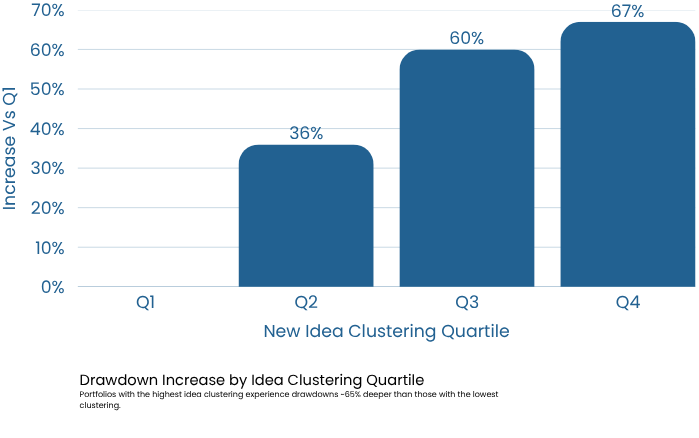

Idea clustering is associated with fragility: many new positions introduced over short periods can lead to deeper drawdowns.

Robustness is structural, not volumetric: this is less about the number of ideas introduced and more about how they enter the portfolio.

Regime shifts reveal structure: changes in market behaviour will stress portfolios and reveal how they are built.

The role of idea generation

When most people evaluate portfolios, their attention is drawn to names already in the portfolio and how they’ve performed. But these are downstream expressions of the investment process, whereas crucial evidence lies in the upstream layer. This is where ideas are generated.

We define idea generation as the process by which stock possibilities come to a manager’s attention before being included in their portfolio.

Of course, we are never privy to the discussions that take place within individual fund groups about potential holdings. The sourcing, debate, and internal filtering of ideas remain largely unobservable. But we can view and analyse these decisions once capital has been allocated to a favoured position – and there’s plenty to examine.

Our research

We analysed 130,000 decision histories from 140 equity portfolios to see how the introduction of ideas affected behaviour. Our goal was to determine whether different patterns of idea generation led to stronger or weaker outcomes.

The focus was on four behavioural dimensions:

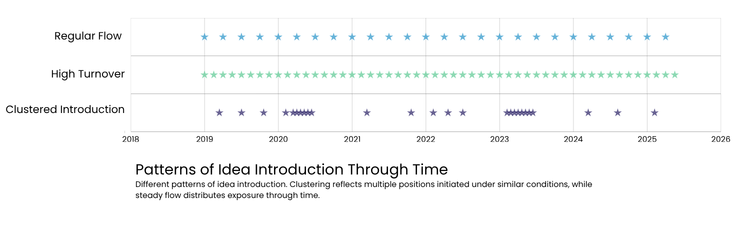

Timing concentration measured whether ideas arrived continuously or in waves.

Idea flow irregularity captured the rhythm of idea generation and whether there was a regular flow of new ideas or if they were sporadic.

Stress reactivity examined whether idea generation accelerates when portfolios come under pressure.

Structural intensity measured the proportion of decisions that introduce entirely new securities, relative to all portfolio decisions.

Our findings

Three key findings stood out:

Idea volume is not informative on its own

Timing structure is more meaningful than activity level

The way ideas enter the portfolio shapes how risk materialises

Idea volume is not informative on its own

The pace at which managers introduce new ideas doesn’t appear to be a meaningful predictor of success. We found that portfolios that generate new ideas frequently don’t enjoy materially higher hit ratios than those that add them more selectively.

In other words, the volume of idea introduction provides limited information about the quality of the investment process, and carries little signal on its own.

Timing structure is more meaningful than activity level

Our research revealed a consistent pattern linked to idea clustering.

Portfolios that initiated many new positions over a short period tended to experience deeper subsequent drawdowns.

This suggests that fragility may be influenced less by the number of ideas introduced and more by the timing of their introduction, particularly when many positions are added under similar conditions.

The way ideas enter the portfolio shapes how risk materialises

Third, we examined how managers behave during periods of portfolio stress.

Drawdowns often place managers under pressure as existing positions are challenged and investment theses are questioned. A natural question is whether ideas introduced during these periods behave differently from those initiated in more stable conditions.

The decision histories analysed don’t indicate that ideas introduced during drawdowns systematically produce weaker outcomes, suggesting that fragility is not primarily driven by deteriorating idea quality under pressure.

The impact on manager behaviour

Our analysis reveals that portfolio behaviour is shaped less by the volume of idea generation than by the structure of how ideas enter the portfolio.

Analysing a manager’s behavioural record – rather than relying on their philosophy – shows structural patterns in how ideas are introduced. The choices made will reveal the boundaries of a manager’s investment universe and how that evolves – or doesn’t – over various time periods.

When ideas are repeatedly drawn from the same sectors or themes over a short period, it can lead to a concentration in a few areas. Conversely, when new names are added incrementally, the various exposures within the portfolio will change more gradually.

Regime shifts

When market conditions change significantly – such as liquidity drying up and correlations between assets shifting – it leads to a regime shift.

When underlying conditions change, positions initiated under similar assumptions may simultaneously come under pressure. It illustrates whether exposure has been accumulated under a narrow set of conditions or built more progressively over time.

Conclusion

New ideas are the lifeblood of successful portfolios, but attention must be paid to how they’re introduced. Adding them to the portfolio in concentrated bursts risks overconcentration and deeper drawdowns. However, a steady flow of fresh opportunities can add alpha to a portfolio without risking its destabilisation.

Decision histories reveal structural patterns. Under scrutiny, robustness is evident not only in outcomes but also in how exposure evolves over time. They also illustrate whether idea flow is continuous or episodic — and that distinction becomes measurable when portfolios are tested.

Robustness, therefore, is less about the number of ideas introduced and more about the patterns by which they enter the portfolio.

About:

The structure of idea generation becomes visible only when decision histories are examined over time, not just through outcomes.

SkillMetrics® analyses how new ideas enter portfolios, identifying whether exposure is built progressively or concentrated under similar conditions.

If you would like to explore how idea flow is structured within your portfolios, we would be pleased to discuss.